- Bitcoin shorts could contribute to higher prices in a short squeeze scenario

- At press time, bulls remained in control despite the recent highs and growing expectations of downside

AMBCrypto previously looked at the possibility of long liquidations if Bitcoin retraces after attaining it most-recent all-time high. Well, despite being overbought, sell pressure remained weak across the board and at press time, BTC holders were still going strong.

One of the main reasons why Bitcoin sell pressure has not taken over is because market confidence was still strong after the recent top. Heavy Bitcoin ETF inflows in the last 24 hours contributed to this. ETF flows have proved to be a relatively accurate measure of market confidence. In fact, according to Bloomberg’s Eric Balchunas,

“HOOVER CITY: Bitcoin ETFs took in a record-smashing $1.4b yesterday (the Trump effect). $IBIT alone was +$1.1b. That’s +$6.7b in past mo and $25.5b YTD. All told they feasted on about 18k btc in one day (vs 450 mined) and are now 93% of the way to passing Satoshi’s 1.1mil btc.”

The surge in ETF inflows may push Bitcoin to greater highs. A recent cryptoQuant analysis recently looked into the possibility of such an outcome forming a short squeeze. According to the analysis, while the Open Interest was high, the funding rates were negative.

Negative funding rates historically indicate a shift in market sentiment, specifically, to a bearish outlook in the derivatives segment. This shift was supported by Coinglass’s BTC long/short ratio which revealed that shorts were higher than longs over the last 3 days.

Source: Coinglass

This surge in short positions was likely because derivatives traders anticipated the previous top to act as a resistance level. Or at least short-term profit taking to trigger another pullback. However, shorts would be at risk of liquidations if the price pushes up.

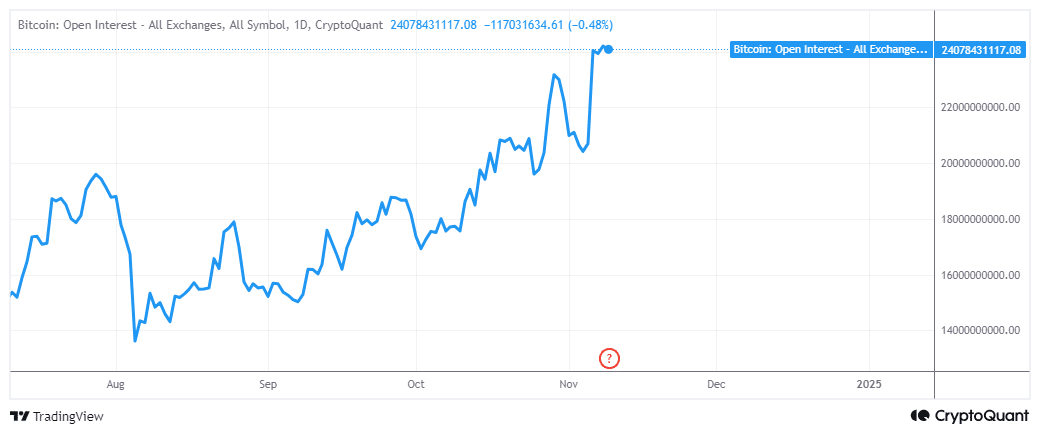

Meanwhile, Bitcoin’s Open Interest appeared to be levelling out after attaining a new ATH. Figures for the same peaked at $24.19 billion on 8 November.

Source: CryptoQuant

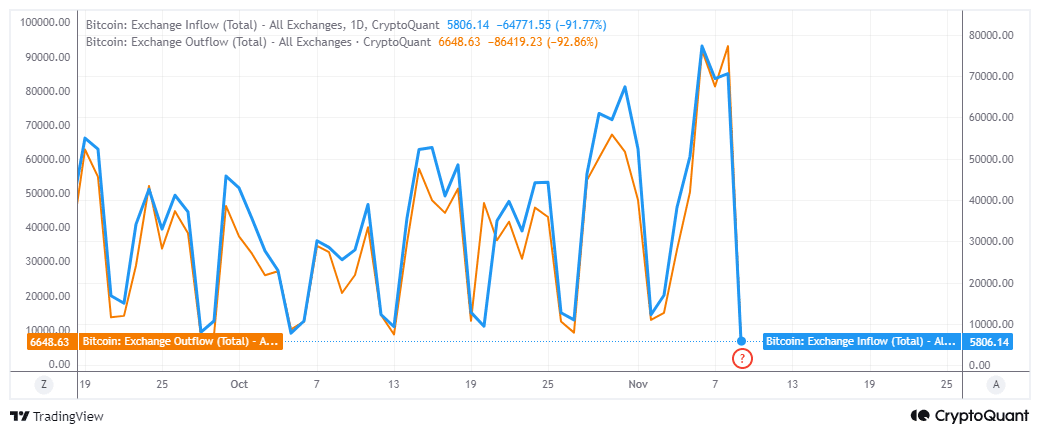

Exchange flows indicate that demand was still higher than sell pressure

Exchange flow data dropped considerably recently, indicating signs of potential bullish exhaustion. Despite this finding, however, the amount of BTC flowing out of exchanges was still slightly higher than BTC exchange inflows.

Source: CryptoQuant

Bitcoin had 6,648 BTC in exchange outflows on 9 November, compared to 5,806 BTC in inflows. This suggested that demand was still in favor of the bulls and the price could still tick up.

Based on the aforementioned data, it seemed clear that there was still some bullish momentum preventing the bears from taking over. This, combined with the demand coming from Bitcoin ETFs, may explain the prevalence of optimism. However, this does not necessarily mean that the situation will remain like that.

BTC’s price action demonstrated that the bulls have been struggling to push higher. This may be a sign that demand is cooling down, which may then pave the way for a bearish retracement once sell pressure starts to gain traction.