Bitcoin is showing a textbook spot-versus-derivatives divergence.

However, how this setup plays out depends on the broader macro environment.

In a risk-on market, higher derivatives activity can support more upside. In a risk-off market, rising leverage increases the risk of a sharp correction. Recent U.S.-Iran uncertainty brought macro FUD back into the market.

However, the Crypto Fear & Greed Index held above extreme fear. That resilience has revived the debate over whether BTC’s bear market could be nearing its end.

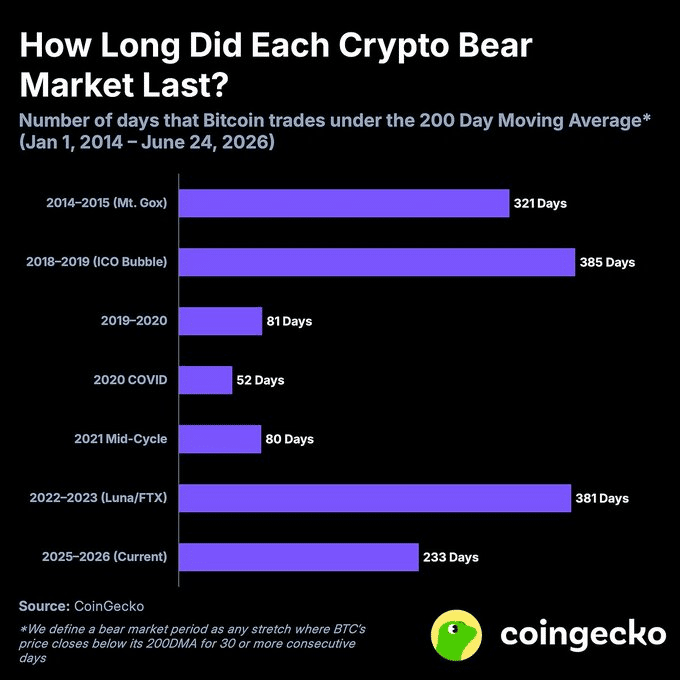

History, however, tells a different story.

As the chart shows, Bitcoin’s current bear market has lasted 248 days. By comparison, the 2022 bear market lasted 381 days, while the 2018 one lasted 385 days, suggesting the current cycle may still have further room to run.

Institutional positioning also supports that view.

As the market flipped risk-off, spot Bitcoin ETFs saw more than $85 million in net outflows after three straight days of inflows, showing how quickly institutions pulled back as macro uncertainty returned.

Bitcoin’s Coinbase Premium Index tells a similar story.

The index has flipped negative, signaling weaker U.S. spot demand and suggesting institutional buyers have become more cautious as risk sentiment deteriorates.

Taken together, the data suggest Bitcoin is still far from a sustained risk-on environment, with the broader bear cycle remaining intact. Against this backdrop, the growing spot-versus-derivatives divergence becomes even more important.

So, what is it telling us about Bitcoin’s next move?

Bitcoin derivatives surge as spot demand lags

In a volatile market, liquidity injections can send mixed signals.

This time, the timing looks more bearish than bullish.

Tether recently minted $1 billion in fresh USDT even as the overall stablecoin market continues to shrink. Rather than flowing into risk assets, much of that liquidity appears to be sitting on the sidelines, suggesting investors are holding dry powder instead of buying Bitcoin.

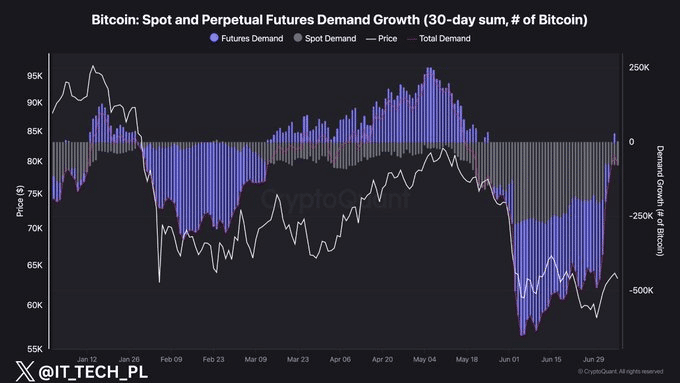

The chart below shows why that matters.

Bitcoin’s 30-day cumulative demand has rebounded sharply from nearly -500,000 BTC to around -75,000 BTC, but the recovery has been driven almost entirely by derivatives. Futures demand has surged from roughly -295,000 BTC to slightly positive, while spot demand remains weak at around -78,000 BTC.

Naturally, that leaves Bitcoin in a clear spot-versus-derivatives divergence.

Against this backdrop, the recent $1 billion USDT injection could add more fuel to Bitcoin’s derivatives market than its spot market.

With speculative positioning already leading the recovery, the fresh liquidity could drive leverage even higher instead of attracting real spot buyers. That would leave Bitcoin’s recovery more vulnerable to a sharp flush if sentiment flips risk-off.

In that context, Bitcoin’s bear cycle still looks far from over. If history is any indication, the current cycle has yet to reach the length of previous bear markets.

Final Summary

- Bitcoin’s recovery is being driven by leverage, while spot demand remains weak, making the rally more fragile.

- With macro uncertainty still high and fresh USDT liquidity entering the market, Bitcoin’s bear cycle may still have further to run.