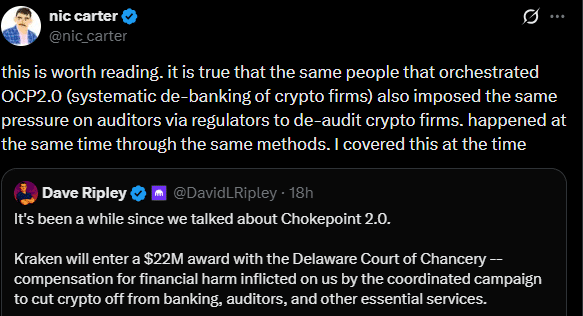

Kraken has secured a major win for the harm it endured during Biden-era industry-wide crypto debanking, popularly known as Operation ChokePoint 2.0.

In a statement, Kraken co-CEO David Ripley said the exchange’s parent company, Payward, was awarded $22 million in damages against its auditor, Mazars. Ripley explained that Mazars abandoned the audit in 2023, citing ‘legal developments’ linked to an SEC complaint.

He noted that there was no professional disagreement, yet Mazars called it quits, exposing the firm to significant losses.

That SEC complaint? Later dismissed with prejudice. No penalties. No changes to our business. But the abandoned audit cost us years and millions in legal fees to clear a cloud we did nothing to create.

Ripley acknowledged that Mazars was pressured, mirroring a broader trend against the crypto industry by the Biden administration.

The firm was not walking away from bad clients. It was walking away from an industry that had become politically expensive to serve. We were the collateral damage.

For him, the targeted restriction did not stop at crypto auditors. In early 2023, banking regulators (the Federal Reserve, FDIC, and OCC) instructed banks to pause support for crypto-related activities, citing safety concerns.

Similarly, the SEC’s SAB 121 guidance made it impossible for banks to get into custody services. Binance, Coinbase, MetaMask, Uniswap, Ripple, and several other crypto startups were affected by lawfare and crypto debanking.

Some of these actions were later reversed by the Trump administration’s executive orders.

Operation ChokePoint: Why crypto could still be at risk

Interestingly, Senator Elizabeth Warren (D‑MA) was a leading voice in efforts to restrict crypto auditors. This was according to venture capitalist Nic Carter, who first covered the Operation ChokePoint 2.0 report in 2023.

Unfortunately, executive orders are not permanent solutions. In fact, they can be overturned by a new president or Congress. This could expose the industry to another round of risks in the future.

Already, Sen. Warren has been questioning some of U.S. President Donald Trump’s push to integrate crypto into the banking sector.

Without formal legislation that addresses some issues raised, the industry is far from being safe from similar risks. Analyst Austin Campbell echoed a similar warning and added,

This continues to be a problem, in that it is still possible and regulatory reforms have not occurred. Nice to see wins here, but more important will be legislative reform and making government employees personally liable for this kind of conduct.

Final Summary

- Kraken received $22 million in compensation for the infamous crypto debanking and de-auditing by Mazars

- Still, the industry could still be vulnerable without formal legislation that prevents a repeat of Operation ChokePoint 2.0