Altcoin

MakerDAO reduces USDC dependency as…

MakerDAO has decreased its dependence on USDC as collateral, shifting focus to Real World Assets (RWA) and experiencing notable growth driven by wstETH.

- MakerDAO reduces USDC reliance, with Real World Assets (RWA) becoming a major collateral source.

- Rising interest in wstETH contributes to MakerDAO’s growth, as DAI’s dominance in the stablecoin sector increases.

Despite facing competition from Lido in the DeFi sector, MakerDAO [MKR] continues to make improvements to its protocol. Recent developments have showcased a decrease in DAI’s reliance on USDC as collateral.

Is your portfolio green? Check out the MakerDAO Profit Calculator

Blast from the past

Previously, USD Coin [USDC] accounted for a significant 51.7% of DAI’s collateral, making it the dominant asset. Meanwhile, Ethereum [ETH] constituted 7.7% of the overall distribution, serving as a secondary collateral option.

Over time, USDC’s contribution to DAI collateral decreased to less than 9%. Real World Assets (RWA) now form a substantial portion, with 25.5% of DAI collateral consisting of various RWAs, including a diverse portfolio of short-term bonds.

This shift demonstrates MakerDAO’s efforts to diversify its collateral and reduce dependency on a single asset.

Source: MakerDAO

The inclusion of RWA not only helps secure DAI as collateral, but also contributes to the overall revenue generation for MakerDAO. By incorporating real-world assets into the ecosystem, MakerDAO expands its potential revenue streams beyond cryptocurrency-related activities.

MakerDAO’s revenue has seen a notable increase of 32.9% in the past week, reflecting the positive impact of strategic changes. Simultaneously, the Total Value Locked (TVL) on the protocol has also experienced a similar rise, indicating growing confidence and activity within the ecosystem.

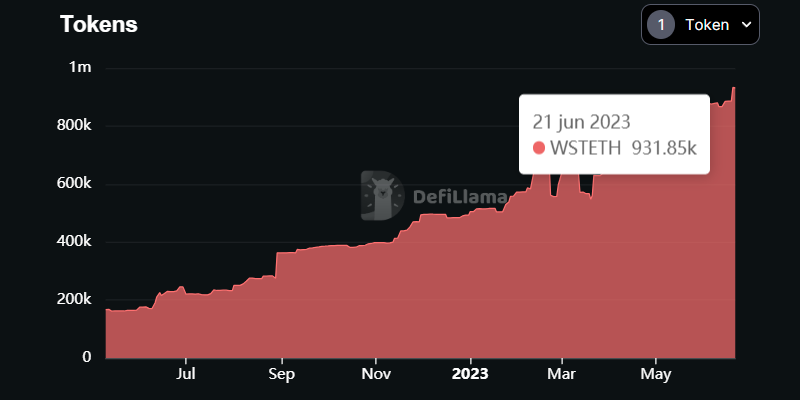

The rising popularity of wstETH among MakerDAO users plays a significant role in the protocol’s recent growth. With approximately 932k wstETH held by the Maker Protocol’s smart contracts, it represented around 46% of the total supply.

Users leverage their liquid-staked ETH holdings through wstETH for DAI loans and on-chain leverage, fostering a symbiotic relationship between wstETH and DAI within the protocol.

wstETH has gained significant traction within the Maker Protocol, closely approaching wETH in terms of Total Value Locked (TVL), making it one of the top collateral options.

Source: MakerDAO

State of MKR and DAI

At press time, MKR was trading at $709.6, after experiencing notable price growth. However, the decline in MKR holdings by large addresses suggested a reduced interest among whales, showing a shift in investment preferences.

Additionally, the number of addresses holding MKR has also decreased during the same period, pointing out changes in the composition of MKR token holders.

Realistic or not, here’s MakerDAO’s market cap in BTC’s terms

While DAI’s dominance in the stablecoin sector has increased, as reflected in its growing market capitalization, its network growth has shown a significant decline.

This decline may imply a slowdown in new address adoption or a temporary decrease in interest from new participants, requiring further examination to understand the underlying factors.

Source: Santiment