Stablecoins aren’t just crypto anymore: $400B in 2025 payments has banks on edge

As stablecoin adoption rises and regulations change, will the broader financial system see co-existence or disruption?

Stablecoins have long been considered the “cash” of cryptocurrency markets, providing a means of trading Bitcoin, transferring liquidity between exchanges, and avoiding volatility without ever leaving the blockchain.

Now, traditional consumers are also embracing stablecoins. In the past year alone, stablecoin frameworks have been introduced by regulators. At the same time, stablecoin rails have been integrated by payment giants, and businesses are experimenting with them for cross-border payments.

Naturally, this has raised an important question: Are stablecoins replacing banks?

Cross-border payment mechanism

To put things in perspective, traditional cross-border payments still depend on pre-funded nostro accounts, SWIFT messaging, and correspondent banks. This makes transfers costly, time-consuming, and opaque.

However, now businesses have a quicker and less expensive way to settle international payments. Stablecoins help complete transfers in seconds and operate 24/7, without the need for correspondent banks or pre-funded accounts.

That benefit is what’s causing adoption.

Metrics supporting the stablecoin adoption race

Mastercard, for instance, agreed to buy BVNK for up to $1.8 billion, Visa’s stablecoin settlement volume reached a multi-billion-dollar annualized run rate by late 2025, and Stripe incorporated Bridge into its payment system.

This proves that banks aren’t being replaced by stablecoins. Although they enhance payment infrastructure, they don’t offer credit creation, lending, or deposit insurance.

According to McKinsey, stablecoin payments totaled about $400 billion in 2025, while tokenized bank deposits are estimated to transfer about $4 trillion yearly.

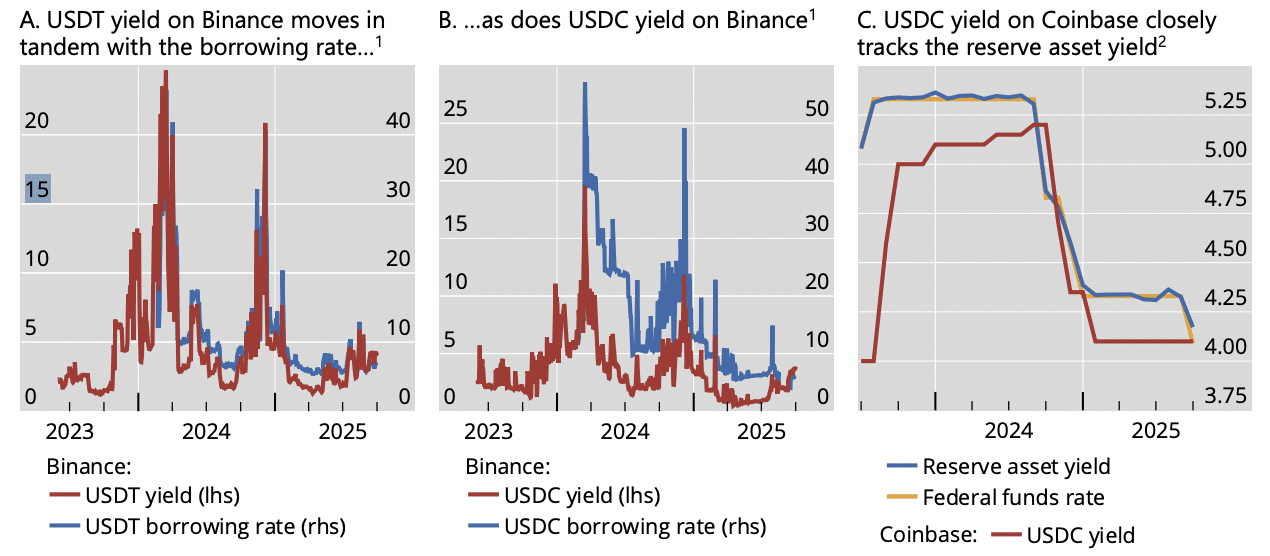

Additionally, only 15% of every $1,000 that is converted into USDC or USDT returns to banks as reserves, which explains why banks are tokenizing deposits to keep funding while increasing blockchain efficiency.

This prompted the Bank of England to relax its planned restrictions on stablecoins.

Mixed opinion from industry leaders

In an email sent to AMBCrypto, Shantnoo Saxsena, CEO and founder of Encryptus, a regulated cross-border payments infrastructure provider, noted,

The Bank of England’s decision to remove individual ownership caps and lower reserve requirements is a welcome step forward, but the £40bn issuance limit suggests policymakers are still focused on the wrong risk.

Although a large portion of demand is driven by cross-border payments, Saxsena thinks that the framework assumes stablecoins primarily compete with domestic bank deposits.

He added,

A £40bn cap on sterling stablecoins may sound generous, but it effectively keeps the infrastructure at pilot scale while dollar stablecoins issued elsewhere are already supporting real remittance flows.

Pablo Hernández de Cos, General Manager of Bank for International Settlements, expressed similar views during his April speech at a Bank of Japan seminar, where he said,

If widely adopted in their current form, stablecoins would pose policy challenges in several areas, ranging from credit provision to monetary policy. For policymakers, it is key to consider how these challenges might differ from those that arise in today’s two-tier banking system.

Stablecoin critics remain

However, in a recent email to AMBCrypto, Maksym Sakharov, CEO and co-founder of WeFi, opposed this viewpoint.

Stablecoins are putting pressure on the weakest parts of cross-border infrastructure: delayed settlement, too many intermediary steps, unclear costs, and slow reconciliation. They make the need for infrastructure improvement harder to ignore.

Additionally, despite his bank developing around the product, Jamie Dimon, JPMorgan’s CEO, has adopted a more skeptical stance. He says he doesn’t understand why anyone would choose a stablecoin over a traditional payment method.

However, he also reiterated that JPMorgan will “be in it and learning a lot” anyhow, operating both its own deposit token and third-party stablecoin rails concurrently.

Where is this going over the next decade?

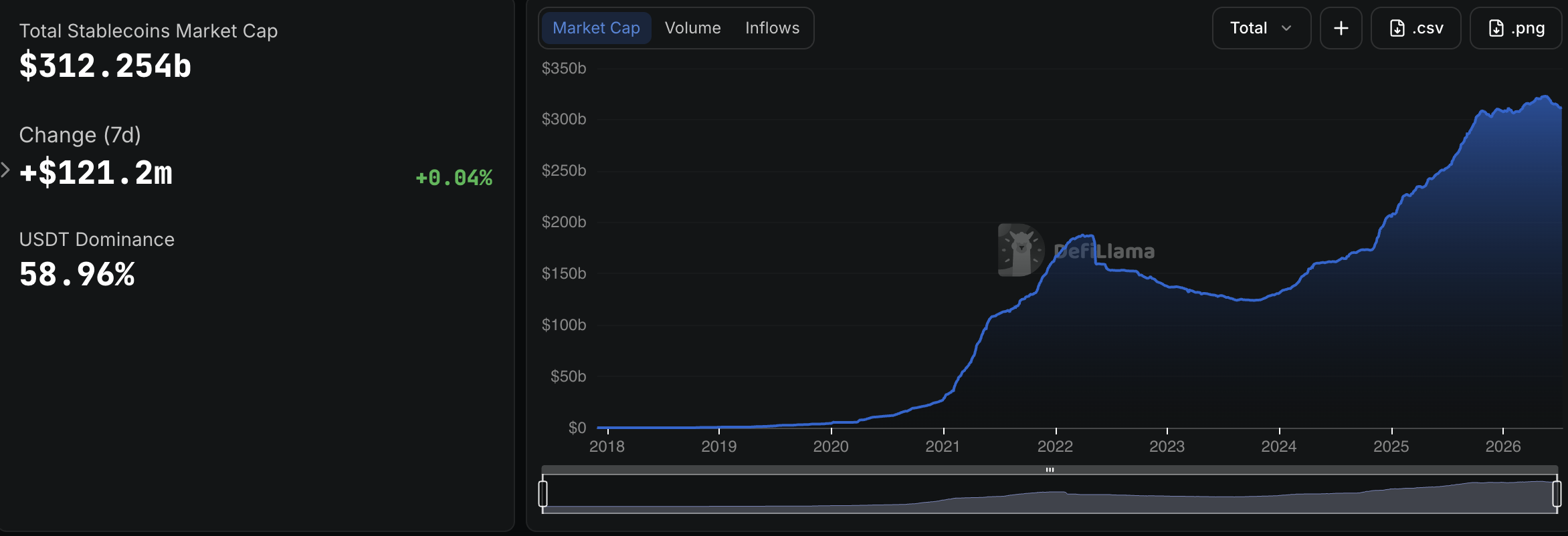

Nevertheless, the stablecoin market cap has already reached $312 billion, with Circle and Tether controlling about 85% of the supply and 99% of it being denominated in US dollars.

Interestingly, it also surpasses the reserves of 95 countries.

Here, Sakharov added what the stablecoin market needs to grow further.

Real adoption is visible when stablecoins solve repeated financial problems. A freelancer getting paid by an international client, a company settling with suppliers, or a business managing treasury across markets is using stablecoins for access, speed, and predictability.

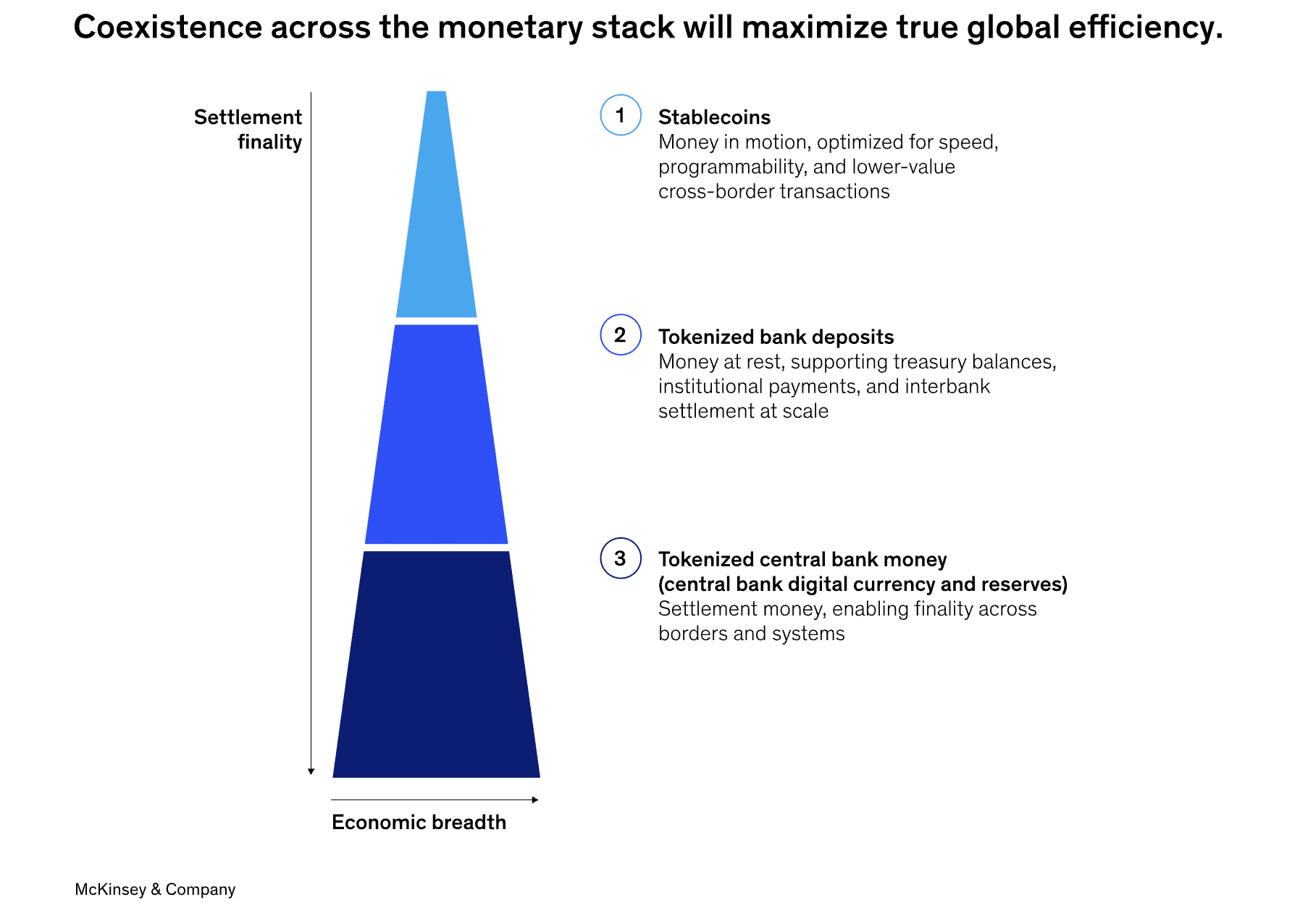

Therefore, it’s safe to conclude that coexistence rather than replacement is more likely the result of the rise of the stablecoin market.

While banks still offer services like deposits, lending, and compliance, stablecoins are taking the place of the expensive, slow payment rails that support traditional banking.

Final Summary

- The stablecoin market has reached a market cap of $312 billion, with Circle and Tether controlling about 85% of the supply.

- Amidst concerns about stablecoins replacing banks, adoption and regulations are shifting attitudes.