Simplify crypto tax loss harvesting with Koinly

Users venturing into the crypto world often find it tiresome to figure out the taxes to be paid on their crypto income. Calculating and filing taxes can be quite complex, especially if users have made transactions in multiple countries. Koinly eliminates all of these complications by automatically consolidating the user’s trades in one location and assisting them in promptly reporting their taxes.

Koinly is a game-changing tax software that streamlines and simplifies cryptocurrency tax filing. The software automatically calculates users’ capital gains and produces a tax report once they link their crypto exchange accounts.

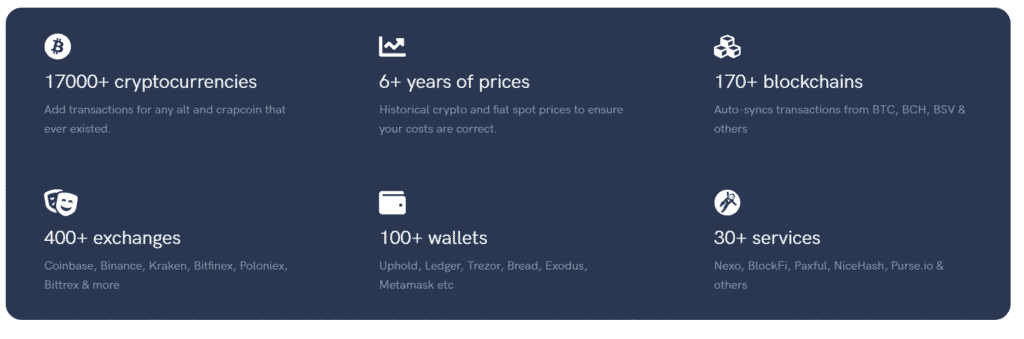

Koinly supports more than 17,000 cryptocurrencies, over 350 exchanges, and 50 wallets, which is more than most of its competitors. This implies that users can connect all of their accounts to Koinly and get a centralized view of their crypto holdings and transactions.

Crypto Tax Loss Harvesting

Any time users sell, swap, spend, or even gift (depending on where they reside) a cryptocurrency, the tax office sees this as disposing of a capital asset, and as a result, the users will incur a capital loss or capital gain.

If users make a capital gain, they’ll have to pay Capital Gains Tax on the profit from their disposal and do not have to pay tax on it if they make a capital loss. When users file their taxes as part of their annual tax return, they deduct their net capital loss from their net capital gain and the amount remaining after that is the amount on which they will pay the Capital Gains Tax.

Crypto tax loss harvesting occurs when an investor sells cryptocurrency at a loss to generate a capital loss that may be offset against capital gains and decrease their overall tax burden. Users may then buy the asset back at the reduced price to HODL it for later gains.

And by tracking the unrealized losses and realized gains, users can keep an eye on their taxable gains throughout the year and look for opportunities to create losses to balance them.

Crypto wash sales

A crypto wash sale is when an investor sells a crypto asset at a loss to create a realized loss and then buys the same asset back immediately at the lower price before the market changes again, creating an artificial loss that can be used to reduce their tax bill.

But tax offices worldwide are sending a clear message that crypto investors need to pay tax on their crypto gains and have set very stringent rules to try and stop investors from pursuing artificial losses.

Each country calls these rules differently, in Australia, it’s known as the wash sale rule.

Australian Crypto Wash Sale Rule

The Australian Tax Office (ATO) has a tax loss selling rule for capital assets. The Australian wash sale rule applies when an investor sells an asset at a loss and purchases the same asset with the intention of a tax benefit. Unlike many other tax offices, the ATO doesn’t specify an exact period and instead states several factors that may constitute a wash sale.

If users are considered to be conducting a wash sale, capital losses as a result of these transactions cannot be claimed and offset against capital gains. The ATO hasn’t specifically stated that these rules apply to crypto but they are general Capital Gains Tax rules and crypto assets are subject to CGT rules.

The ATO issued a warning to taxpayers in June 2022, asking them not to engage in wash sales, implying that it will be a priority for them this tax year. According to the ATO, taxpayers who engage in wash sales are at risk of facing swift compliance action and potentially additional tax, interest, and penalties.

Assistant Commissioner Tim Loh said,

“Don’t hang yourself out to dry by engaging in a wash sale. We want you to count your losses, not have them removed by the ATO.”

Australia’s Capital Loss Limit

In Australia, users can use capital losses to offset capital gains. Although there is no limit, customers are required to spend all of their capital losses each year before carrying any further. As a result, if users still have a net capital gain for that fiscal year, they are not permitted to carry the capital losses forward.

Users can carry over capital losses indefinitely to future fiscal years if they have greater capital losses than what they can utilize in a single fiscal year.

The crypto tax loss harvesting deadline in Australia is from 1st July 2021 to 30th June 2022.

Tax loss harvesting crypto with Koinly

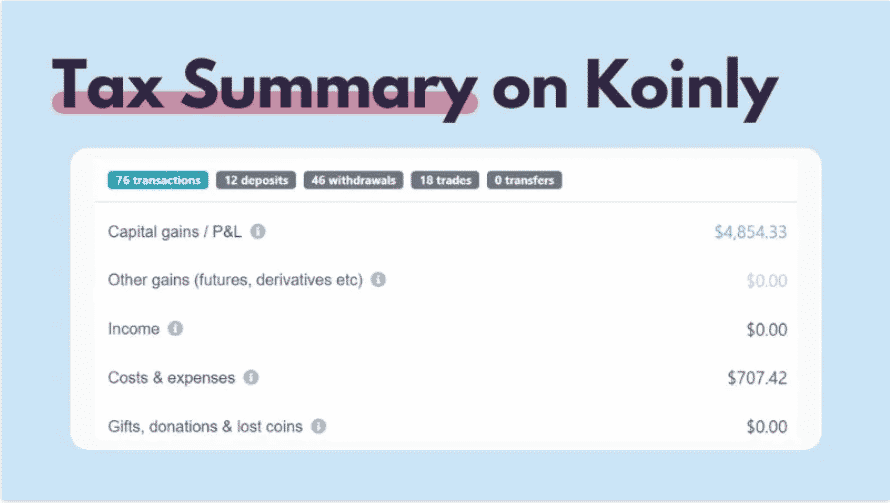

A user needs to set up a free account and sync all of the existing crypto wallets and exchanges used. Koinly then determines the short- and long-term capital gains, capital losses, cryptocurrency income, and any other expenses. The user can view all of this information on the tax report page in the summary, which provides a comprehensive representation of the tax bill for the fiscal year.

Koinly also lets users track their unrealized profits and losses in the dashboard. Users will be able to monitor the performance of each of their crypto assets and spot potential possibilities for tax loss harvesting.

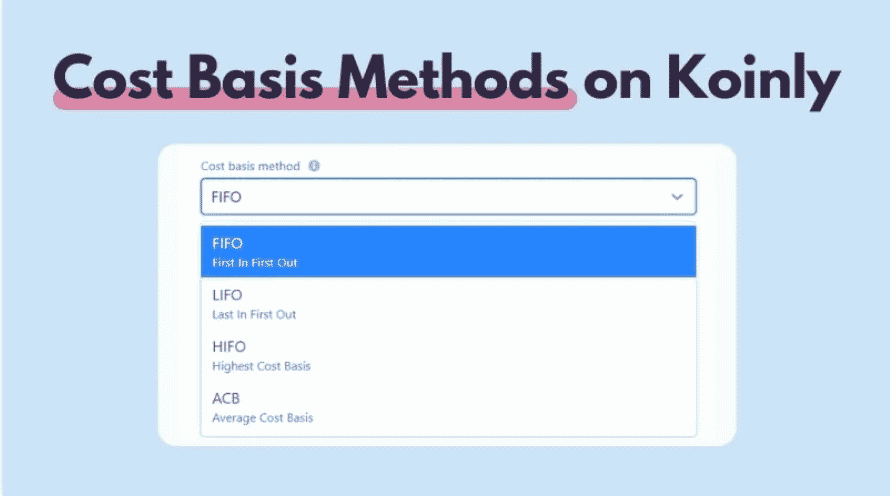

Koinly sets up the cost basis method based on the user’s location. For example, the share pooling cost basis method for UK users or the average cost basis method for Canadian users. For countries where there is a variety of cost basis methods available, like the US and Australia, Koinly uses FIFO by default. However, customers may also choose in the settings which cost basis approach they want to apply.

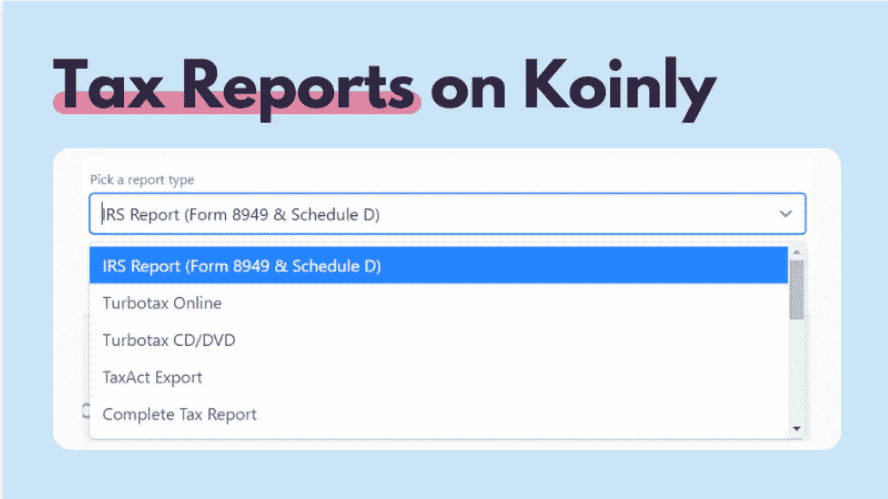

Finally, users have to go to the tax report page and pick the tax report they want to download. Koinly offers specific tax reports based on where the user’s location. For example, the IRS Schedule D and Form 8949 for US taxpayers or the HMRC Capital Gains Summary for UK taxpayers.

Final Word

Koinly offers an effortless solution to monitor crypto investments and simplify tax reporting. With features like portfolio tracking, easy data importation, error reconciliation, and reliable crypto tax reports, the platform is a great crypto taxation tool for people searching for a simple way to handle their taxes.

Readers can get a 20% discount on any Koinly subscription by using the promo code AMB20.

To know more about the platform, visit its official website.

Disclaimer: This is a paid post and should not be treated as news/advice.