Why sticking it to Coinbase, Ripple isn’t the best move from the SEC

SEC Chairman Gary Gensler visited the Aspen Institute for a conference this summer and made it clear that the rules were “awfully clear” on digital assets. He said something similar in a recent interview with the Financial Times, urging blockchain and fintech developers to “talk to us, come in!” The fate of the industry, like all finance, is about trust, he added.

Encouraged by these words, one of the biggest companies in the crypto-industry, Coinbase, moved in for guidance on their new product.

What happened next? Well, Coinbase was slapped with a Wells Notice faster than it could say ‘regulatory clarity.’ This is now yet another chapter in the SEC’s love-hate relationship with cryptocurrency organizations. This time, however, it might be more personal than what meets the eye.

Brief flashback in 3, 2, 1…

As reported previously by AMBCrypto, the United States Securities Exchange Commission (SEC) recently served Coinbase with a Wells Notice on a silver platter. A Wells notice is how a regulator tells a company that it intends to sue the company in court. The notice in question came on the back of Coinbase’s ‘Lend’ program. Needless to say, Coinbase CEO Brian Armstrong is at his wit’s end.

On Twitter, Armstrong claimed the threat of legal action came as a surprise since the organization has been speaking to the SEC for weeks before its lending product launch. Now, while many in the community are empathizing with Coinbase, it is hard to look past the level of naivety displayed by the public company.

I mean, what did you expect, Brian? A kiss and good luck greetings from the most ambiguous regulators in the United States?

SEC’s Coinbase reaction is not surprising

Adding Coinbase to its list of dissatisfied customers, it is not at all surprising that the SEC has continued to go on the offensive against cryptocurrency-related organizations. Regulators have often maintained their apparent ‘high horse’ opinion that the sheer size of the digital asset ecosystem compels them to make sure these operations lie within the ambit of existing laws and guidelines.

However, Ripple is standing right on the side, and the SEC hasn’t played exactly by the rules.

According to Armstrong, Coinbase was not provided with any conclusive explanation as to why their lend program or their potential lending contract is being looked at as securitization of an asset, in this case, USDC. It resonates fairly well with the fact that the Commission also denied Ripple’s motion to prove its Howey test application.

In fact, the SEC gloriously responded that Ripple did not like the answers they received, hence, they were pushing ahead with the motion.

But, aren’t regulators supposed to explain the reasoning behind such lawsuits? Coinbase execs are pondering over the same question, just like Ripple a few months back.

Additionally, the SEC also demanded the exchange provide customer information from its Lend program waiting list. This is the SEC trying to breach privacy violations, further lending credence to the impression that anti-crypto sentiment is popular among key policymakers.

An ulterior motive to protect the traditional financial system?

Before dipping our toes into that narrative, here is a recap of what the Coinbase Lend program is all about.

The proposed plan is that the exchange will allow its customers to lend their USDC on the platform, in return for 4% annual interest.

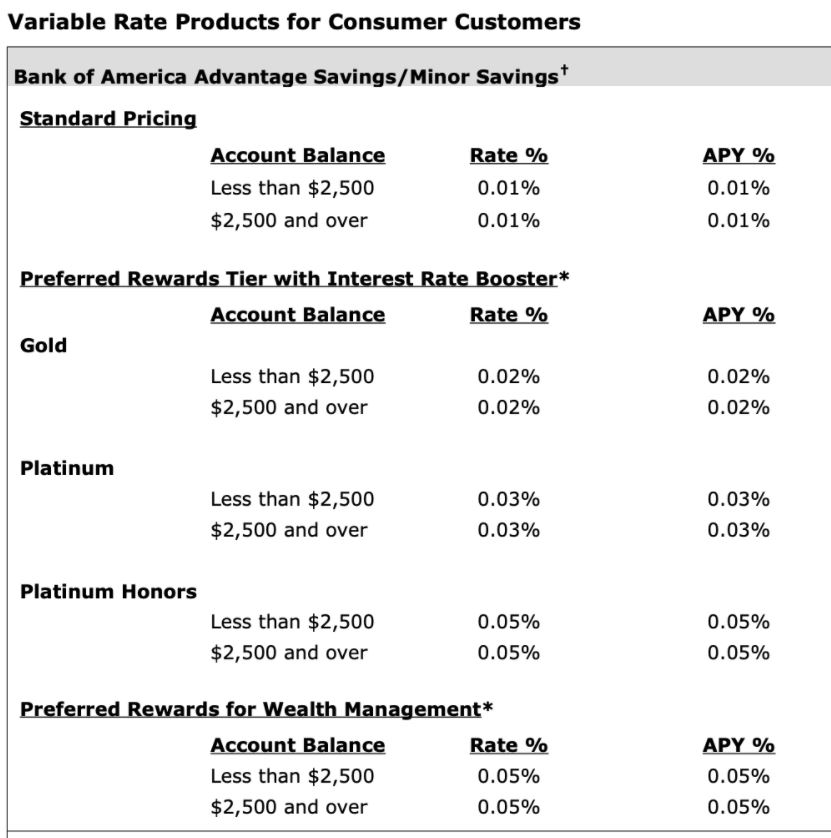

Now, USDC is a cryptocurrency, but it is also a stablecoin. Hence, its value is more or less $1 at all times. Now, a 4% annual interest doesn’t sound like a lot. However, for comparison, here is the breakdown of variable rate products for consumer customers at the Bank of America.

As illustrated above, the annual interest offered by Coinbase is much higher than Bank of America. According to data, 4% annual interest is 8 times higher than the national average for saving accounts in the United States.

Now, it is easier to understand why the SEC would want beef with unregulated crypto-companies. Especially when their beloved banks are facing the threat of capital outflows.

Coinbase is currently offering higher annual interest than banks and it is also a publicly listed company. Its quarterly trading volumes of $500 billion can be enough to bring potential customers to its Lend program. This would invariably result in capital flows from banks to crypto-assets. The SEC may be ambiguous, but the agency and its execs are not stupid. In fact, they have likely identified the bigger picture.

The SEC’s legal action against Coinbase might also be an indication of upcoming federal enforcement against crypto-lending. And, what better way to send a message than going after the blue-chip brand of Coinbase?

Are Coinbase’s hands clean though?

Without sounding like a cheerleader for the exchange, it is imperative to follow both sides of a story. Now, it might be technically incorrect to suggest Coinbase’s arguments about lending hold up against being a securitized asset. As far as U.S securities laws are concerned, a lending contract can be proven as a security but the way SEC has conducted the matter can be considered out of line.

However, here is the potential hook. According to David Canellis, the SEC and Coinbase have been having these conversations for about 6 months now. That is at least a month before the company went public in April 2021.

Now, speculations are rife that Coinbase might have known earlier that its lending program will fall under the security banner.

Coinbase had to go public before launching the lending program because the credibility of being publicly listed obviously goes a long way.

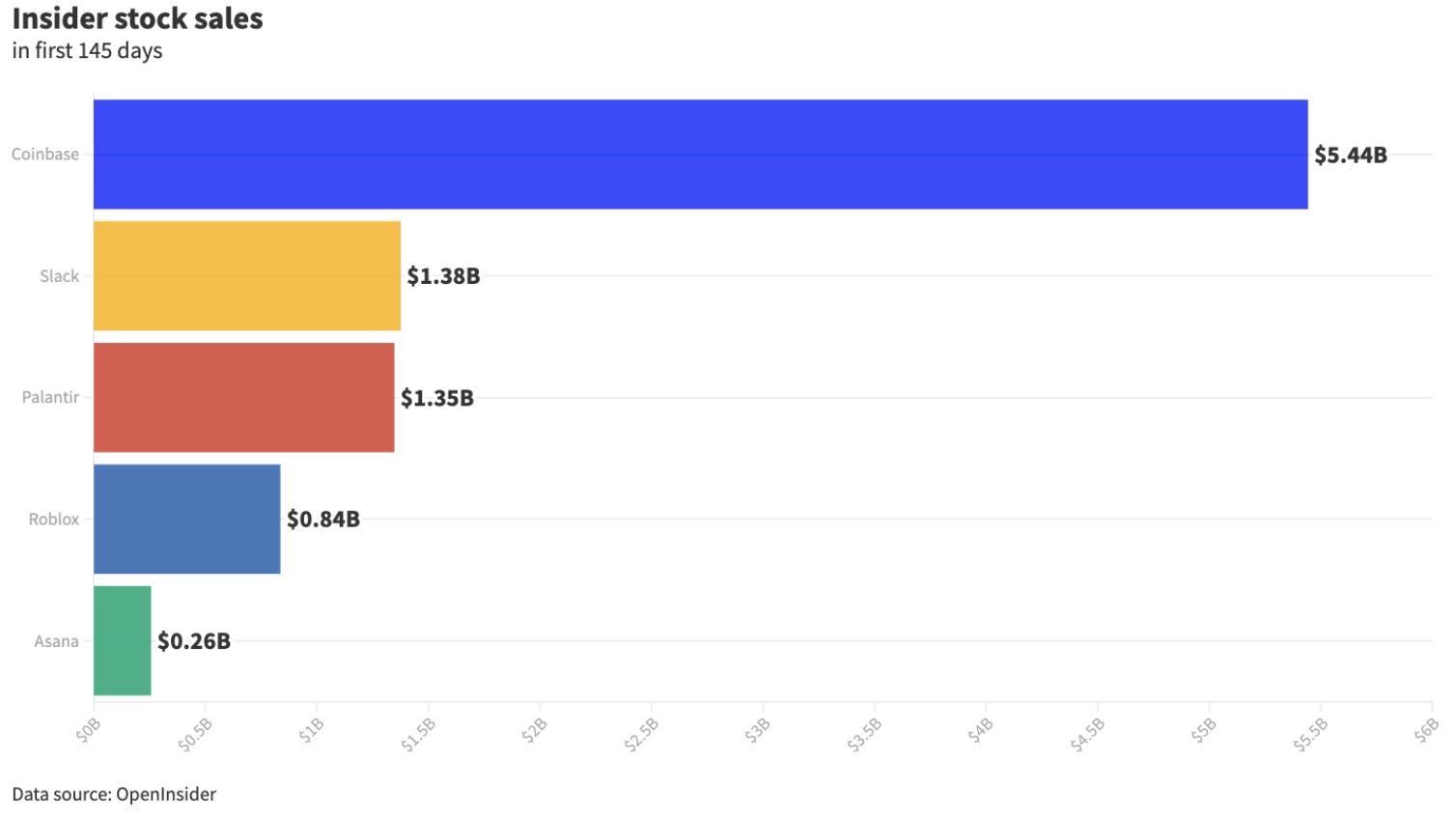

Consider this – With respect to insider stock sales, early Coinbase investors dumped $5.44 billion worth of stock in retail within 145 days. That is 5 times more than the recent list of companies launching their IPO.

Hence, Coinbase execs’ arguments that they had no idea about the lawsuit until recently may be fallacious. The SEC hasn’t responded to those claims yet, so there is still something to look out for though.

No one wins the feud

Global financial innovation is currently at risk with the SEC-Coinbase feud. It is not often you have billionaire investors like Mark Cuban indicating that the SEC’s actions can lead to trillions of dollars being lost in economic benefit for the United States.

That is definitely true.

While Coinbase’s hands may not be clean here, it is also unfair to suggest that the lending program is wrong or immoral. Coinbase is propagating a properly-vetted process for their investment program so that they can disassociate USDC from any type of price volatility. Such cryptocurrency products may help the general investor bridge the gap between existing investors.

It is not a ‘rich getting richer situation’ anymore. Without such options, a majority of the population is left with nominal zero-interest bank accounts. Those aren’t great alternatives either.

SEC’s episodes with Coinbase and Ripple are reflective of the rigid financial regulatory system. The SEC ain’t winning any brownie points by stamping its authority since the likes of Coinbase will continue to push the boundaries of fintech and crypto-upheaval.